Homeowners refinance their mortgages for an assortment of reasons. Some reasons center around strictly wanting to pay off their homes faster and at better interest rates, while others may fall along practical life events or emergencies. If you find yourself asking, “should I refinance my mortgage,” try checking off a few boxes to help come to a decision.

Here are a few reasons folks may refinance their fixed rate mortgage:

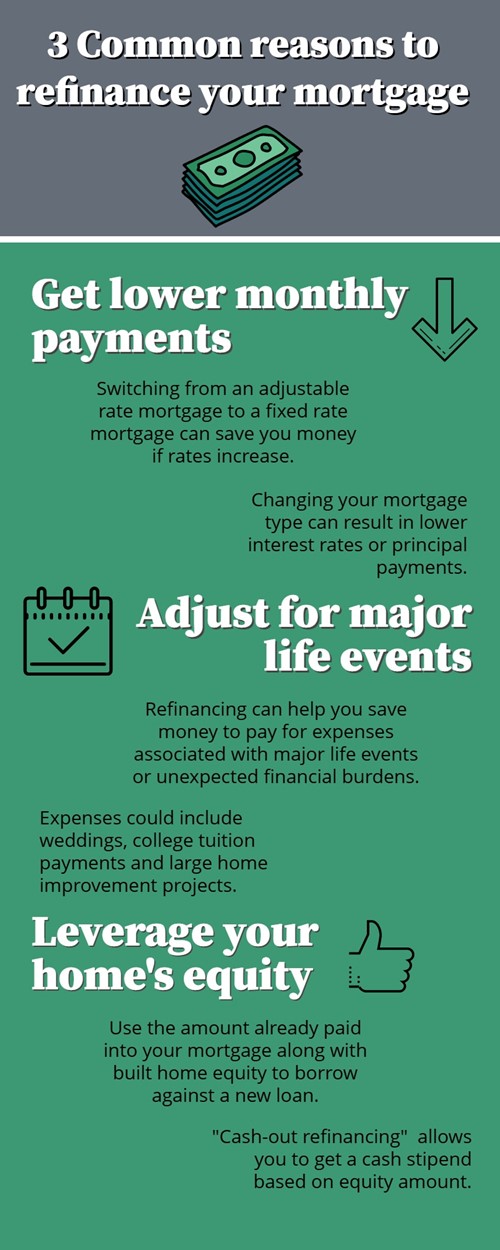

Lower monthly payment

One of the more upfront reasons to refinance a mortgage is to make your monthly mortgage payments more affordable. Some may even seek to reduce their monthly payments by switching their mortgage interest type from an adjustable rate mortgage to a fixed rate mortgage, especially if the interest rates start to creep higher than anticipated.

You’ll want to consider your current loan term against the refinanced loan term to determine if adding extra years or higher principal payments is worth refinancing before jumping into a new mortgage. Sometimes, the monthly savings fall below the lifetime savings of the loan and may not be worth the extra refinance fees.

However, if you find refinancing your mortgage puts you in a great financial place, and you don’t have any large changes in income or expenses coming your way, it may be a perfect time to refinance.

Life events

Sometimes, you may find you want to refinance your mortgage for life events such as weddings, school tuition, large home improvements or other personal expenses. If you find yourself in an emergency, you may also want to consider refinancing.

Regardless of your life event, consult your current mortgage lender to ensure you can refinance without breaking any terms or conditions set forward by the original agreement. If you can refinance, be sure to keep your finances as close to budget as possible, so you don’t end up with more debt or financial hardships than is necessary.

Home equity

After you’ve paid a decent amount into your mortgage loan, and have built some equity in your home, you can borrow more than your outstanding mortgage balance and receive the difference.

For example, if you’ve paid $50k into your current mortgage, with $150k outstanding, and want to refinance for a lower interest rate while getting more out of your home equity, applying for a new mortgage loan may be a great option. You could request $200k while using your home’s equity as a primary component for your new fixed rate loan.

Taking advantage of a “cash-out refinance” or “cash-out refi” gives you $50k to be placed back in your pocket for whatever projects or payments you want to use it for. Meanwhile, your new refinanced monthly payments may stay the same or lower, depending on the lender.

When refinancing your home, be sure to check in with your mortgage lenders. Some will offer you the options you’re searching for without having to switch to a new company that may not have your information on file or may request something deeper.

However, if you find a mortgage lender that checks all of your boxes, try contacting one of their loan officers to explore your options.

About the Author

Ryan Christensen

Responsive, Responsible and Resourceful - How Real Estate Should Be. This is the foundation of our continued success: responsive service, providing accurate and timely information, and demystifying the process. 100% of my business is referral based because I listen to my clients' needs and exceed their expectations. As a full-time real estate broker, I am the best advocate for both my buyers and sellers. I am always available, regardless of the time of day.

Being a native Southern Californian is a tremendous advantage. I know the area. Time is more valuable than money, but neither can be wasted. And, I'm a fan of hard work. My clients can enjoy their home buying and/or selling experience because I provide a trusting, focused, straightforward approach. I look forward to helping you achieve your goals and find joy in homeownership.

I am both a licensed Real Estate and Mortgage Broker. Others choose to concentrate on one or the other. I provide a higher level of service and expertise than those who do not obtain this dual skill set, which differentiates me from other service providers. My decisions and advice are based solely on what is in the best interest of my clients. I use Real Estate Sales as a tool to make sure my clients get the home that meets or exceeds their needs. As a Mortgage Broker, I search for the best loans so I can offer lower rates and pricing than my financing competition. This certainly IS in the client's best interest.